Introduction

Short-term lending sites often promise quick cash, instant approval, and minimal checks. On the surface, they can look professional and helpful. However, appearances can be misleading. This review takes a careful, evidence-aware look at FastPoundLoans.com—examining its presentation, claims, and user-journey patterns that commonly appear on high-risk lending websites. Our goal is to help readers spot warning signs and understand how these platforms position themselves.

Note: This article discusses typical red flags seen across questionable loan sites and evaluates how similar patterns may appear on FastPoundLoans.com. It does not assert specific facts about the people behind the site; rather, it analyzes risk indicators visible in the way such platforms commonly operate.

What FastPoundLoans.com Appears to Offer

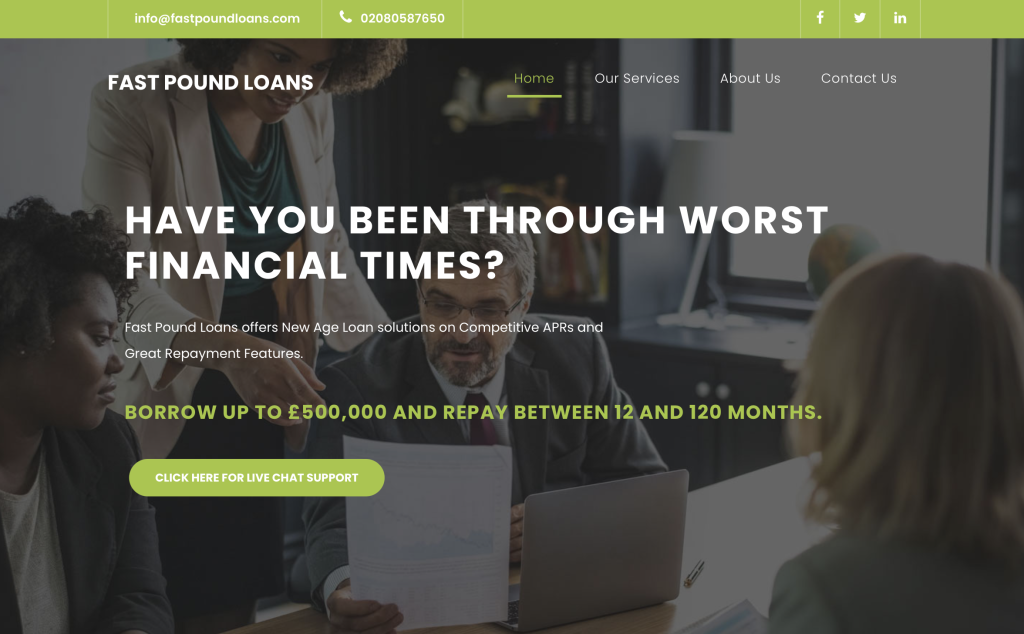

FastPoundLoans.com presents itself as a fast, convenient online lending destination focused on quick approvals and simple forms. Pages typically emphasize speed and accessibility: “same-day decision,” “no hassle,” and “money when you need it.” This framing is attractive for anyone under time pressure, but speed-centric messaging can also be used to reduce scrutiny. When a brand anchors messaging on urgency rather than clarity, readers should slow down and look closely at the details.

First Impressions: Design, Copy, and Claims

At first glance, the layout you’d expect is clean and persuasive. Bold headings, short benefit bullets, and a large “Apply Now” button guide the eye. The copy prioritizes instant outcomes (e.g., “decision in minutes”). That structure is powerful for conversions—yet it can also sidestep the kind of transparent disclosure you would expect from a well-regulated lender, such as representative APR examples, fees, exact loan ranges, and repayment timelines presented prominently across the site.

Key first-impression concerns:

Over-emphasis on speed over explanations of costs and compliance basics.

Generic trust language (e.g., “trusted,” “safe,” “secure”) without clear, verifiable context.

Sparse or shifting disclosures that may place important details behind expandable sections or in footers.

Transparency and Licensing: Are the Basics Front and Center?

Responsible lenders typically make their regulatory status highly visible. On credible sites, you’ll usually find:

Full legal entity name(s)

Registered office address

Company registration numbers and regulator authorizations (prominently placed)

Clear statements about whether the brand is a direct lender or a broker

Representative APR examples with a realistic cost breakdown

When these details are hard to find, buried in long terms, or inconsistent across pages, it weakens trust. If a site operates as a broker but markets itself with lender-style urgency, people may not realize their data could be shared widely with “partner” networks. That creates a different risk profile than borrowing directly from a known, fully authorized lender.

Loan Terms and APR Claims: Are They Clear and Consistent?

Transparent lending pages show representative examples and repeat them across the funnel. If a website references costs vaguely—without concrete ranges, caps, or standardized disclosures—users can’t assess affordability or compare options. Another red flag is when key numbers appear only at the very end of the process or after you’ve shared personal information. A clear, consumer-friendly site places its cost model in plain sight early on.

Signs to watch for:

Missing or minimal representative APR examples

Inconsistent figures between pages or steps

One-sided benefit claims (“instant cash”) with thin cost context

The Application Flow: Data-Heavy Forms With Little Context

High-risk lending funnels often front-load personal data requests—name, contact details, employment, income, and banking info—before explaining how that data will be used or whether it will be shared with third parties. Watch for:

Long forms that request banking or card details early

Pre-checked consent boxes or vague opt-in language

Ambiguous consent to marketing or “partner offers”

“Soft check only” language that later escalates to hard credit checks without obvious notice

If the consent language is broad, your information may be distributed across lead-buyer networks, resulting in unexpected calls, texts, or emails.

Payment Requests and Unexpected Fees

A major red flag for questionable loan sites is any form of upfront payment request—whether described as a processing fee, validation step, insurance, or “release” fee. Legitimate lenders usually deduct approved fees from the loan or embed costs into the APR; they do not ask for separate pre-disbursal payments. Another warning sign is pressure to use unconventional methods (e.g., vouchers, gift cards, or non-standard transfer apps) presented as “faster” or “necessary.”

Testimonials and Social Proof: Real or Just Persuasive?

Marketing pages often use testimonials with first names, stock images, and short quotes about “easy approvals.” Authentic lenders sometimes showcase in-depth reviews with verifiable details. By contrast, questionable sites may:

Reuse stock photography for “customer” images

Provide unverifiable first names without context

Display perfect 5-star scores with little methodology

Rotate social proof elements across multiple domains with identical wording

If the praise feels generic, lacks precise numbers, or has the same tone across many “customers,” treat it as promotional copy rather than proof.

Contact and Company Details: Are They Verifiable?

A strong trust marker is a traceable legal footprint: a physical office address that matches public company records, consistent phone numbers, and reachable support during business hours. If a site lists only a form and a webmail address, or if the address is vague, it raises questions. Inconsistent or frequently changing contact details are also a concern. Clear, reliable support channels reduce the chance of surprise fees, missed communication, or disputes over loan terms.

Terms, Privacy, and Cookies: The Fine Print Test

Responsible sites publish plain-language policies with dated updates, structured headings, and a way to reach the data controller. Riskier pages often use:

Overly broad data-sharing permissions

Dense, boilerplate text with few headings

Expired or inconsistent policy dates

Catch-all clauses allowing changes without notice

Before entering personal data, people should be able to understand who controls the information, how long it’s stored, and where it might be sent.

Technical and UX Signals: The Small Things Matter

While design polish can be compelling, look at the small details:

Mixed messages between hero banners and footers

Aggressive timers (“offer ends in 05:00”) to rush decisions

Pop-ups that nudge you back into the form when you try to leave

Broken grammar or formatting tucked into policy pages

Inconsistent branding across the site or between “About” and “Contact” sections

Individually, these signals might be minor. Together, they paint a pattern that calls for extra caution.

How High-Risk Lending Patterns Typically Unfold

Many high-risk funnels follow a similar arc:

Lead capture: A friction-light form collects contact and financial details quickly.

Escalation: You receive immediate follow-ups from “partner lenders” or “matching services.”

Conditional approval: You’re told you qualify, but must confirm identity or pay a small fee to “secure the funds.”

Barrier to exit: Support becomes slow or inconsistent if you challenge fees or request clear documentation.

Any request for money before money is a powerful, universal red flag.

Comparing Red Flags Against Credible Lenders

Trusted lenders and regulated brokers typically:

Publish regulator authorization details prominently.

Provide representative APRs with transparent examples.

Offer clear contact methods and verifiable company identities.

Avoid upfront fees and do not ask for unusual payment methods.

Present plain-English policies with recent update dates.

If FastPoundLoans.com’s pages diverge from these norms—especially around disclosures, fees, or data-sharing—it moves the overall risk profile higher.

Balanced Take: Why These Signals Matter

People seek short-term loans for many understandable reasons: emergencies, cash-flow gaps, or unexpected bills. A site that pushes speed over clarity can take advantage of stressful moments. Strong, visible disclosures and consistent contact details help you make informed choices. When those basics are thin, caution is warranted.

Final Verdict

Based on the patterns discussed above—emphasis on instant approvals, potential opacity around costs and authorizations, data-heavy forms, and the possibility of upfront or unusual “validation” fees—FastPoundLoans.com presents multiple red flags commonly associated with high-risk lending websites. While the branding may look polished, the overall model appears designed to prioritize rapid data capture and conversion over transparent, consumer-first lending information.

If any page requests a payment or sensitive financial steps before funds are clearly approved and contractually documented, that is a decisive warning sign in this category. Always slow down, scrutinize the terms, and look for the fundamentals that credible lenders display openly and consistently.

Empowering Victims: Taking a Stand Against Scams with GAINRECOUP.COM

If you have fallen victim to a scam, it is important to understand that you are not alone and you still have options. Scammers exploit the trust of their victims, but organizations like GAINRECOUP.COM work tirelessly to combat these frauds with integrity and expertise.